The Stock Market Crash of 2025 and the 'Reciprocal' Tariff Myth

There’s nothing reciprocal about these tariffs.

It’s been quite a week. I feel like I went to sleep and woke up in 1930.

Markets continue to crash in response to Trump’s “Liberation Day” tariffs, which were even worse than I imagined.

In the Washington Examiner, I wrote on Trump’s folly.

“Trump, like the protectionists of old, has said all he wants is ‘a level playing field’ because numbers are ‘so disproportionate, they’re so unfair.’ This ignores the reality that the U.S. ranks 69th in the world in trade freedom and has higher trade barriers than most of its trading partners.” (read the entire article here)

But Pete Earle points out that there is nothing “reciprocal” about these tariffs.

“The formula calculated tariffs based on the ratio of trade deficits to total imports, penalizing countries with the largest trade imbalances. This approach deviates from traditional ‘reciprocal tariffs,’ which typically involve matching foreign tariff rates. Instead, it appears designed to reduce the US trade deficit by raising the cost of imports, ostensibly encouraging domestic production while severely disrupting supply chains.”

Watching fortunes vanish and retirement accounts get wiped away is hard to watch. But it’s made worse by the fact that the White House lied about the “reciprocal” nature of these tariffs.

There’s nothing reciprocal about them. If the tariffs were reciprocal, the administration wouldn’t have slapped a 17 percent tariff on Israel, which recently dropped all tariffs on US imports.

For a deeper dive into how the formula really works, Kevin Corinth and Stan Veuger break it down at AEI.

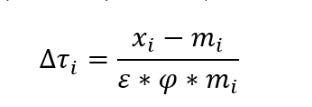

“Though in effect the formula for the tariff placed on the United States by another country is equal to the trade deficit divided by imports, the formula published by the Office of the US Trade Representative has two additional terms in the denominator that just so happen to cancel out: (1) the elasticity of import demand with respect to import prices, ε, and (2) the elasticity of import prices with respect to tariffs, φ.

A lot of what they write will appear as jargon to lay readers, but what’s important to know is that the formula is based “on the response of retail prices to tariffs, as opposed to import prices.”

Corinth and Veuger describe this decision as a “mistake,” and others, including Nate Silver, have cited it as evidence that the White House “applied their stupid f*cking formula incorrectly.”

This is possible, but I think it’s unlikely. It makes far more sense to me that the White House intentionally used the formula because it resulted in higher tariffs (see below) on its trade partners.

Whether the White House was incompetent or deceptive is something readers can decide for themselves. What matters is that America ended up with an average effective tariff rate of 22 percent, “the highest level recorded since 1909.”

You read that correctly. Trump’s tariffs are higher than those of the Smoot-Hawley Act of 1930, the one that sank the United States into the worst depression in its history.

Trump wants to be a great president. If he continues down this path, he’s more likely to be remembered as a Herbert Hoover than a George Washington.

(Bonus: Listen to me discuss tariffs with Bob Harden)

I'm not going to argue with you, but at 50 and having a father who lived through the Great Depression and liked to talk politics, I have never heard of tariffs being *the cause* of the Great Depression until this moment in time. That strikes me as . . . odd.

As I watch this tariff drama unfold, I rarely see anyone mention in their condemnation of the tariffs how over valued the market had become over the past 15 years or so. Standard acceptable P/E ratios have been out the window for a long time now. The affect on the market was due regardless. The tariffs just hastened the fact!